Paying Capital Gains on the Sale of Your Home- That profit from your home sale might not be taxable income

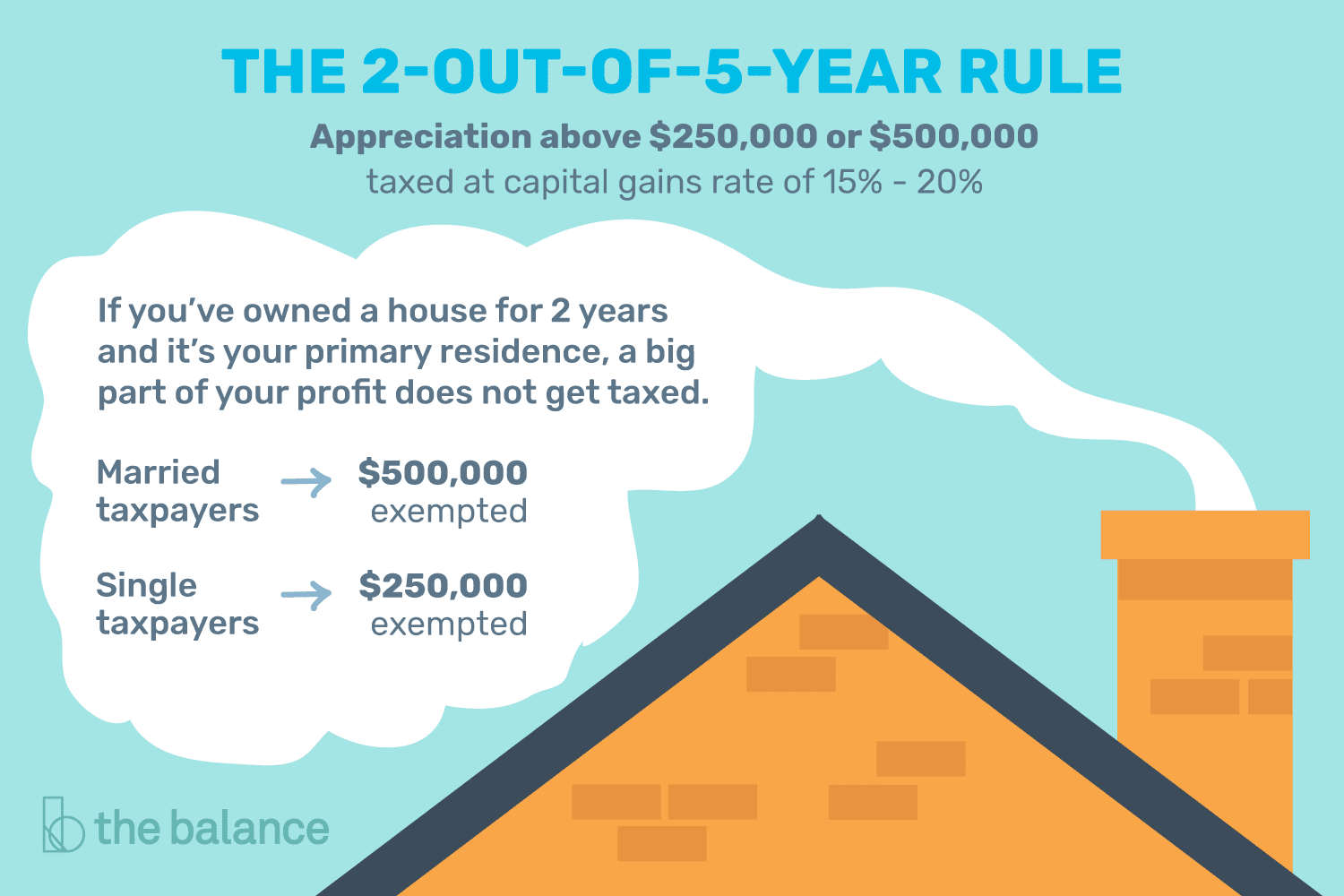

Unmarried individuals can exclude up to $250,000 of profits from capital gains tax when they sell their personal residences, thanks to a home sales exclusion offered by the Internal Revenue Code (IRC). Married taxpayers can exclude up to $500,000 in gains.

Let's say you list your house for sale and fortune smiles on you. You sell it for a tidy profit, then you realize that you might have to give a sizable percentage of that profit to the Internal Revenue Service (IRS) in the form of capital gains tax. But that might not happen because a good many taxpayer.

How Does the Home Sale Exclusion Work?

You would have a gain of $200,000 if you purchased your home for $150,000 and you've sold it for $350,000. You wouldn't have to report any of that money as taxable income on your tax return if you're single, because $200,000 is less than the $250,000 exclusion amount you're entitled to.

Now let's say that you sold the property for $405,000. Your gain would be $255,000 in this case: $405,000 less your $150,000 basis. You would have to report a $5,000 capital gain on your tax return for the year because this is $5,000 more than the $250,000 exclusion.

© The Balance, 2018

Of course, there are rules. You must qualify for the exclusion.

Claiming the home sales exclusion depends on the property being your primary residence, not an investment property. You must have lived in the home for a minimum of two out of the last five years immediately preceding the date of sale. The two years don't have to be consecutive, however, and you don't have to live there on the date of the sale.1

You can live in the home for a year, rent it out for three years, then move back in for 12 months. The IRS figures that if you spent this much time under that roof, the home qualifies as your principal residence.

You can use this 2-out-of-5-year rule to exclude your profits each time you sell your main home, but this means that you can claim the exclusion only once every two years because you must spend at least that much time in residence. You cannot have excluded the gain on another home in the last two-year period.2

Exceptions to the 2-Out-of-5 Year Rule

You might be able to exclude a portion of the gain if you lived in your home less than 24 months but you qualify for one of a handful of special circumstances.

You can calculate and claim a partial home sales exclusion based on the amount of time you actually lived in the residence if you qualify under one of the special rules.

Count the months you were in residence, then divide the number by 24. Multiply this ratio by $250,000, or by $500,000 if you're married and you qualify for the double exclusion. The result is the amount of the gain you can exclude from your taxable income.

For example, you might have lived in your home for 12 months, then you had to sell it for a qualifying reason. You're not married. Twelve months divided by 24 months comes out to .50. Multiply this by your maximum exclusion of $250,000. The result: You can exclude up to $125,000, or 50% of your profit.

You would include only the amount of your gain over $125,000 as taxable income on your tax return if your gain was more than $125,000. For example, you would report and pay taxes on $25,000 if you realized a $150,000 gain. You could exclude the entire amount from your taxable income if your gain was equal to or less than $125,000.3

Qualifying Lapses in Residency

You don't have to count temporary absences from your home as not living there. You're permitted to spend time away on vacation or for business or educational reasons, assuming you still maintain the property as your residence and you intend to return there.2

And you might qualify for a partial exclusion if you're forced to move due to circumstances beyond your control. For example, you could exclude a part of your gain if your work location changed so you were forced to move before you'd lived in your house for the qualifying two years. This work exception would apply if you started a new job, or if your current employer required you to move to a new location.3

Document your condition and the situation with a statement from your physician if you're forced to sell your house for medical or health reasons. This, too, allows you to live in the home for less than two years yet still qualify for the exclusion. You don't have to file the letter with your tax return, but keep it with your personal records just in case the IRS wants confirmation.

You'll also want to document any unforeseen circumstances that might force you to sell your home before you've lived there the required period of time. According to the IRS, an unforeseen circumstance is "an event that you could not reasonably have anticipated before buying and occupying your main home."3

Natural disasters, a change in employment or unemployment that left you unable to meet basic living expenses, death, divorce, and multiple births from the same pregnancy would all qualify as unforeseen circumstances under IRS rules.

Active duty service members aren't subject to the residency rule. They can waive the rule for up to 10 years if they're on "qualified official extended duty." This means the government ordered you to reside in government housing for at least 90 days, or for a period of time without a specific ending date.

You'll also qualify if you're posted at a duty station that's 50 miles or more from your home.1

The Ownership Rule

You must also have owned the property for at least two of the last five years. You can own it at a time when you don't live there, or you can live there for a period of time without actually owning it.

Your two years of residency and the two years of ownership don't have to be concurrent.

For example, you might have rented your home and lived there for three years, then you purchased it from your landlord. You promptly moved out and rented it to another individual, then you sold it two years later. You've met both the ownership and the residency two-year rules because you lived there for three years and owned it for two.2

Service members can waive this rule as well for up to 10 years if they're on qualified official extended duty.1

Married Taxpayers

Married taxpayers must file joint returns to claim the exclusion, and both must meet the 2-out-of-5 year residency rule, although they don't have to have lived in the residence at the same time. Only one spouse must meet the ownership test.2

The home sales exclusion isn't available to married taxpayers who elect to file separate tax returns.

A surviving spouse can use their deceased spouse's residency and ownership time as their own if one spouse dies during the ownership period and the survivor hasn't remarried.4

Divorced Taxpayers

Your ex-spouse's ownership of the home and time living in the home can count as your own if you acquire the property in a divorce. You can add these months to your time of ownership, as well as to your time of residency, in order to meet the ownership and residency rules.4

Reporting the Gain

The income on the sale of your home is reported on Schedule D as a capital gainif you realize a profit in excess of the exclusion amounts, or if you don't qualify for the exclusion. The gain is reported as a short-term capital gain if you owned your home for one year or less. It's reported as a long-term capital gain if you owned the property more than one year.

Short-term gains are taxed at the same rate as your regular income, according to your tax bracket. The rates on long-term gains are more favorable: zero, 15%, or 20%, depending on your tax bracket.5

The 20% long-term capital gains rate doesn't apply unless your overall taxable income is $434,550 for more as of 2020 and you're single, or $488,850 if you're married and filing a joint return. The IRS indicates that most taxpayers pay no more than the 15% rate.5

Keeping accurate records is key. Make sure your realtor knows that you qualify for the exclusion if you do, and offer proof if necessary. Otherwise, your realtor must issue you a Form 1099-S recording your profit and send a copy to the IRS as well. This won't prevent you from claiming the exclusion, but it could complicate things and you might need the help of a tax professional to straighten it out.

You must report the sale of your home on your tax return if you receive a Form 1099-S. Consult with a tax professional to make sure that you don't take a tax hit that you don't have to take.

Calculating Your Cost Basis and Capital Gain

The formula for calculating your gain involves subtracting your cost basis from your selling price. Start with what you paid for the home, then add the costs you incurred in the purchase, such as title and escrow fees and real estate agent commissions.

Now add the costs of any major improvements you made, such as replacing the roof or furnace. Unfortunately, painting the family room doesn't count. The key word here is "major."

Subtract any accumulated depreciation you might have taken over the years, such as if you ever took a home office deduction. The resulting number is your cost basis.6

Your capital gain would be the sales price of your home less your cost basis. You've had a loss if it's a negative number. Unfortunately, you can't claim a deduction for a loss from the sale of your main home, or any other personal property.

You've made a profit if the resulting number is positive. Subtract the amount of your exclusion and the balance, if any, is your taxable gain

https://www.thebalance.com/sale-of-your-home-3193496